US

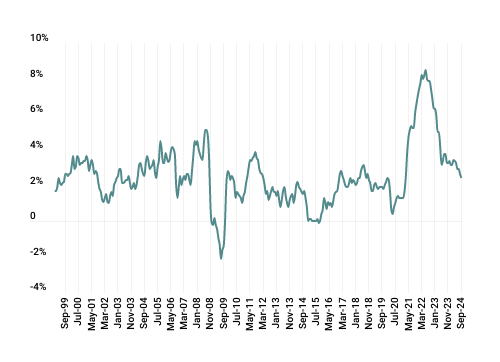

Markets ended the quarter on a high note, as easing inflation allowed policy makers to re-shift their focus towards sustaining growth. Questions about when and by how much the Federal Reverse (the Fed) will cut rates were answered, as the central bank announced its first rate cut since the COVID pandemic. Negative mid-quarter data regarding unemployment and manufacturing activity raised concerns that the US economy may be slowing down and heading towards a hard landing; however, favorable retail sales and inflation data in August alongside higher-than-expected Q2 GDP growth raised hopes that the “soft landing” scenario is indeed achievable.

The Federal Open Market Committee (FOMC) met in July and September. The July meeting was not notable, but in September all but one voting FOMC member agreed to reduce the federal-funds target rate corridor by 50 basis points (to 4.75-5.00%); the lone dissenting voice voted for a reduction of 25 bps. The decision to cut by 50 bps (as opposed to a more typical 25 bps) was framed as follows: 1) in order to keep the economic expansion on track; 2) real overnight interest rates are well above the “neutral” rate, even after the cut of 50 bps. In the Summary of Economic Projections (SEP), by the end of 2024, the median Fed expectation for unemployment is an increase from 4.0% to 4.4%, while the expectation for PCE inflation is a decrease from 2.6% to 2.3%. Additionally, and probably most impactful, were the reductions to the median Fed expectations for the federal funds rate at the end of 2024 and 2025, from 5.1% to 4.4% and 4.1% to 3.4%, respectively.

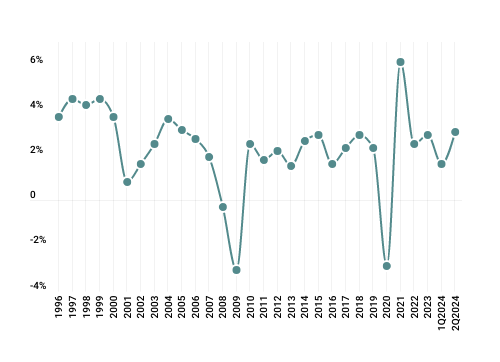

In recent quarters, US business investment activity has shown resilience and growth. Real non-residential fixed investment has grown at a consistent rate of 4-6% per year since 2021, outperforming historical trends and forecasts. In Q3 2024, business investment was predicted to rise by 4.2%, slightly down from 4.5% in 2023, driven by investments in structures, machinery, equipment, and intellectual property. Capital expenditures have been boosted by factors such as AI projects and domestic manufacturing reshoring. Despite elevated interest rates, many firms have continued to invest due to strong returns on capital and available cash reserves.

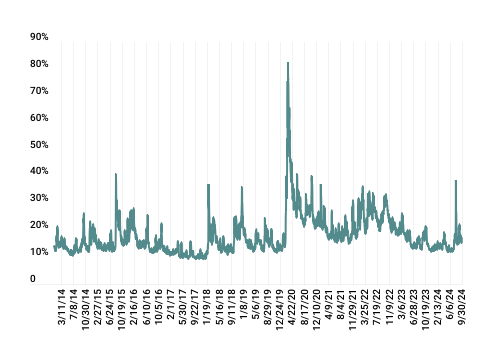

Commercial real estate continued to face challenges across various sectors during the quarter but displayed some signs of stabilization amid expectations for lower interest rates. The MSCI RCA CPPI National All-Property Index gained 0.6% in August, marking its fourth consecutive monthly rise, and showed a slight year-over-year gain of 0.2%. While the industrial and retail sectors experienced growth overall, the office and multifamily sectors continued to lag.

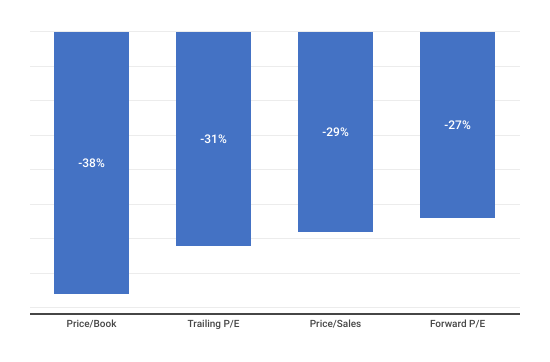

The office sector experienced the steepest declines in value amid rising vacancies and delinquencies. Over the last year, office property values have declined 9.6%, with a notable contrast between those located in central business districts (CBD) and the suburbs. The value of CBD office properties has declined 27.4%, whereas suburban office properties have declined just 4.7%. Over the last three years, the sector’s overall decline reached 20%, with CBD experiencing a staggering 51.3% decline, compared to just 13.3% in suburban areas.

![UnderConstruction_shutterstock_415850113 [Converted]](https://www.crewcialpartners.com/hubfs/UnderConstruction_shutterstock_415850113%20%5BConverted%5D.png)