US

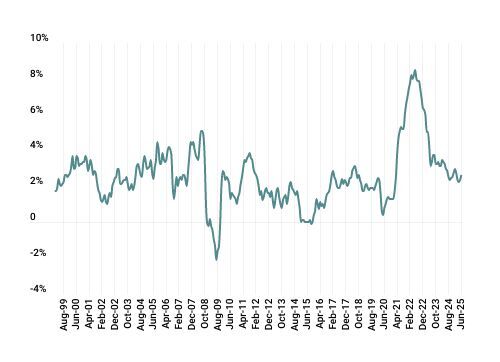

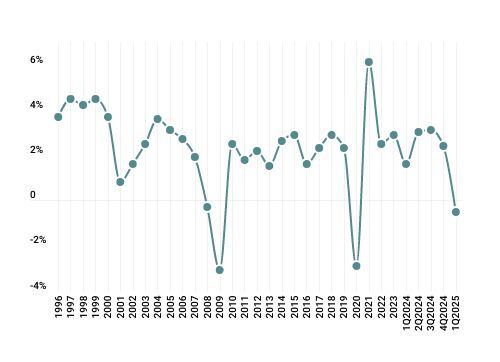

US financial markets started the quarter in disarray after the Trump administration announced sweeping tariff reforms. On April 2, a new baseline 10% tariff on nearly all imports was announced, with additional country-specific "reciprocal" rates added on top, either replacing or increasing preexisting rates. The Budget Lab at Yale estimated the average effective tariff rate would increase from below 3% to more than 22%, the highest level since 1909. However, in the ensuing weeks, many of these rates were lowered, setting the stage for the S&P 500 to rebound to new highs (the shortest recovery time for the S&P 500 following a 15% correction on record). At the end of the quarter, the Budget Lab’s average effective tariff rate estimate was reduced to slightly above 15%, still the highest level since 1934; the lab estimates that these tariffs have the potential to decrease domestic real GDP growth by 60 basis points per annum through 2035.

Traditional safe-haven assets failed to respond predictably: the US dollar and treasuries remained volatile until mid-May, stabilizing only after a US/China détente. Some economists suggest capital markets themselves may have pressured the administration to walk back parts of the tariff schedule, citing weakening confidence in the dollar, foreign capital flight, and shrinking trade imbalances.

The Federal Reserve held rates steady at 4.25–4.50% amid uncertain growth and inflation outlooks, while downgrading its economic projections for the second straight quarter. Futures markets now imply a 3.7% federal funds rate by year-end, below the Fed’s forecast, anticipating two or more cuts. The Fed’s balance sheet declined by $100 billion to $6.7 trillion.

Commercial real estate showed tentative signs of stabilization, though office space, particularly in central business districts, remains under pressure. National office vacancy reached a record 20.6%, with CBD office values down 51.8% over the past three years. Suburban office fared better, while multifamily housing declined 18.4% over the same period. In the residential market, conditions are gradually normalizing. Home price appreciation slowed to a 13-year low of 1.8% as inventory improved, though affordability remains constrained. Performance has become increasingly regional, with the Midwest and Northeast showing gains while many Sunbelt markets experienced price declines. Rising mortgage rates, property taxes, and insurance costs continue to weigh on demand.

![UnderConstruction_shutterstock_415850113 [Converted]](https://www.crewcialpartners.com/hubfs/UnderConstruction_shutterstock_415850113%20%5BConverted%5D.png)