11 min read

ACTIVE MANAGEMENT: THE CASE FOR SKILL IN AN UNCERTAIN MARKET

There are currently more than 60 armed global conflicts around the world, the most of any period since World War II, most recently punctuated by...

8 min read

Crewcial Partners : June 4, 2026

Crypto, the gamified economy, and the cost of mistaking momentum for value

“Brian: You’ve got to think for yourselves! You’re all individuals! Crowd, as one: Yes! We’re all individuals!” Monty Python’s Life of Brian (1979)

There is a moment midway through Monty Python’s Life of Brian when the crowd decides it has found ultimate meaning. The man at the center—Brian, who is not a messiah and says so, repeatedly and earnestly—cannot shift them. His resistance only deepens their conviction. A discarded gourd becomes a holy relic, a lost sandal becomes another, and the crowd promptly splits into warring factions over which object is the truer sign. It does not hear what Brian is saying; it hears what it has already decided to believe. Born next door to Jesus on the same night, Brian is mistaken not for anything he has done, but because proximity to the real thing is enough for belief to do the rest. Once belief starts moving, it feeds on itself.

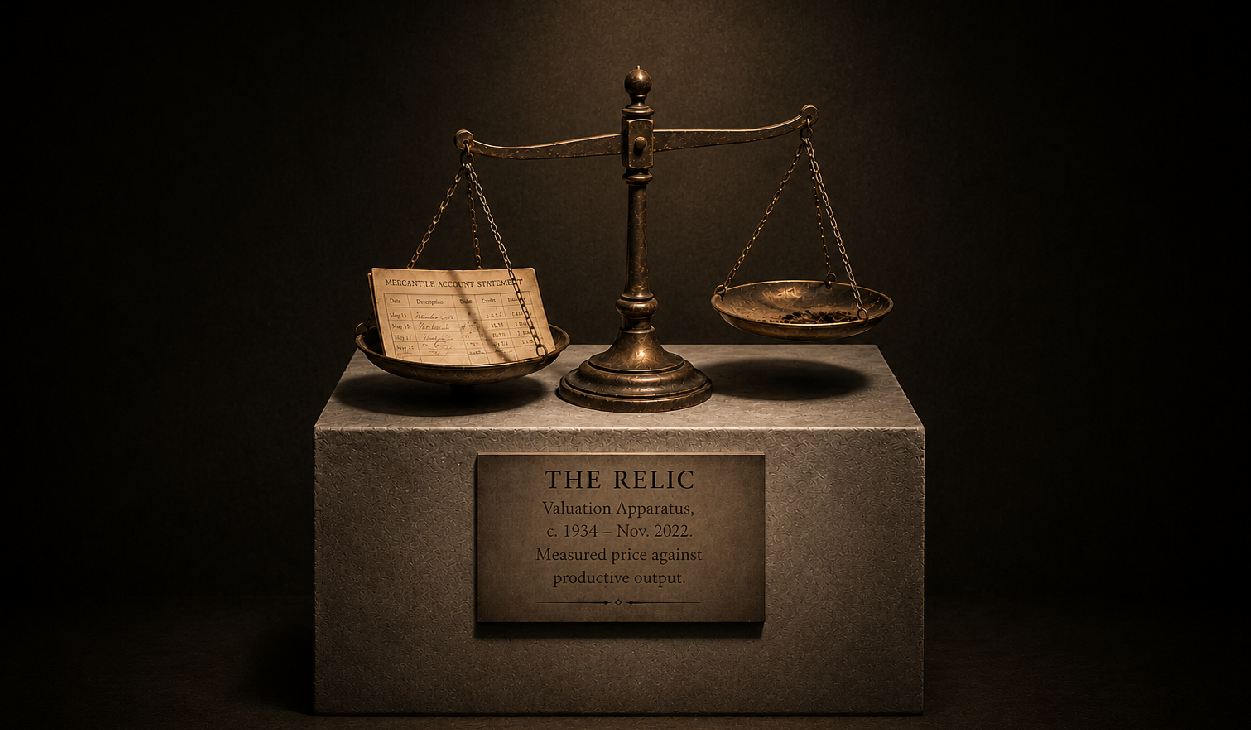

For most of modern financial history, markets were designed to resist that impulse. Prices were imperfect, often flat-out wrong, but they were at least trying to reflect reality, in a constant shimmy towards truer valuation. Earnings and cash flows mattered, while fundamentals ensured a certain baseline gravity.

That assumption still exists, it is simply much weaker than it used to be. What is replacing it is not mass irrationality per se, though that is a factor, so much as gamification at scale: an economy increasingly shaped by feedback loops, hype cycles, and self-reinforcing collective behavior, where rewards flow not to those who are right or durably innovative, but to those who arrive early and leave fast. Crypto did not invent this dynamic (it is more catalyst than prime mover), but it has stripped away the remaining illusions for the discerning investor, while Big Tech and the AI story thrive in the same liminal space. At its core, the gamified economy runs on a familiar fuel we’ve discussed before: FOMO. That fear of missing out is not a side effect. It’s the engine.

Markets, like crowds, want stories. Tokens do not promise ownership of productive assets. They promise participation in a narrative. Rising prices validate the story, which draws in more participants. The loop closes.

In October 2025, a record liquidation event wiped out more than $19 billion in leveraged crypto positions in 24 hours as Bitcoin and a swath of altcoins plunged. Over 1.6 million traders were forced out of positions as liquidity vanished and margin calls accelerated the sell-off. This was not a fundamental reassessment, but a narrative reversal. Once the story shifted, the crowd moved.

These collapses are driven less by changes in utility than by liquidations, narrative, and leveraged positioning. It is no anomaly; it’s nature of the game. When the score stops rising, players do not debate fundamentals; they run for the exit, often taking unwilling competitors with them.

According to CoinGecko, more than half of all cryptocurrencies ever created have failed or gone inactive. These projects did not fail because the underlying technology broke. Simply, attention moved on. That is speculation behaving like entertainment.

The same logic has extended beyond crypto. Meme stocks, equities that go viral on social media rather than as a result of changes in business fundamentals, returned with notable force in 2025. Opendoor Technologies surged roughly 245% in July 2025 despite reporting a net loss, driven entirely by social media momentum and short-squeeze mechanics rather than any improvement in its home-flipping business. Kohl’s surged more than 100% intraday in a single session with nearly half its float sold short, as coordinated retail activity on Reddit and X forced a short squeeze with no material change to the underlying business.

Meme Stock Mania 2.0 cannot be dismissed as mere nostalgia; this must be considered an evolved, structurally embedded market dynamic. In April 2026, Allbirds surged more than 580% in a single session after announcing a pivot to AI compute infrastructure, rebranding as NewBird AI, despite having sold its core footwear business for $39 million weeks earlier. Retail net buying hit a record single-day high of $5.2 million, even surpassing demand on its 2021 IPO day. The stock gave back the majority of those gains within 48 hours. And GameStop, the original meme stock, remains structurally embedded in this dynamic five years after its first short squeeze, its price still predominately tethered to sentiment cycles and social media catalysts beyond any underlying business performance.

But the same impulse driving these retail flows perhaps finds its purest financial expression elsewhere, in zero-day options, contracts that expire the same day they are traded. By September 2025, 0DTE options exceeded 60% of total US stock options volume, a structural threshold that had never previously been crossed. Retail traders’ share in short-dated options rose from around 35% to 56% over the same period. These are highly leveraged bets on intraday narrative moves, placed by participants who are not asking what a business is worth but which direction sentiment will move in the next six hours; they cannot be considered hedges in the traditional sense. CME Group data shows same-day expiry contracts on the S&P 500 more than doubled in volume over the past four years. This has moved beyond niche behavior towards a structural feature of how prices are now formed.

FOMO is no longer incidental. It is structural. Platforms reward early entry, rapid movement, and constant engagement. The implicit message is simple: hesitation is costly.

The issue is not necessarily illegality, but distortion: capital misallocated at the expense of productive investment and valuation discipline. The question for long-horizon investors is whether the market’s price formation function is still performing the role it was designed to perform, or whether it has been significantly compromised by mechanisms optimized for engagement rather than accuracy.

Every game needs characters. Heroes, villains, visionaries. Tech culture has always produced outsized personalities, but the gamified economy turns them into economic accelerants. Individuals become representative of cultural signaling. Symbols become investment theses. And eventually, criticism becomes disentangled from honest debate and re-categorized as heresy.

This is how you get the “bros.”

Elon Musk tweets and markets move. Peter Thiel’s worldview has become shorthand for entire investment strategies and quasi-religious movements. Palantir CEO Alex Karp’s The Technological Republic, a sweeping techno-nationalist manifesto that became an instant #1 New York Times bestseller in 2025, illustrates how the CEO-as-prophet role has expanded beyond commentary into an explicit pitch for a new political economy organized around defense-tech primacy, with Palantir’s own contracts the implicit endpoint; that Palantir’s stock trades at a trailing P/E exceeding 200 suggests the market has already priced in this sermon.

Techno-futurist narratives, such as AI salvation, crypto liberation, and Mars colonization, blend ambition with an idea of inevitability. Buying the asset becomes an act of faith as much as analysis. This is not accidental. Academic research on speculative manias shows that social reinforcement and charismatic leadership can materially amplify bubble dynamics, especially when assets lack clear valuation anchors. Prices rise not because information improves, but because belief spreads. From Charles Ponzi to John Law, from the radio-era promoters of the 1920s to the dot-com visionaries of the late 1990s, the mechanism is consistent: belief concentrates first in people, then in prices.

The AI story has followed this arc with particular intensity. JP Morgan Asset Management has noted that AI-related stocks have accounted for 75% of S&P 500 returns, 80% of earnings growth, and 90% of capital spending growth since ChatGPT launched in November 2022. OpenAI is now valued at $852 billion, a figure its own backers have begun to openly question, despite cumulative losses now projected to reach $115 billion through 2029. Its CEO has publicly stated he believes an AI bubble is underway. The crowd heard the first part, but it’s still working through the second.

The circular financing that has emerged in this environment is worth examining directly. OpenAI took a stake in AMD while Nvidia invested $100 billion in OpenAI; Microsoft is a major customer of CoreWeave, in which Nvidia holds an equity stake; Microsoft accounted for nearly 20% of Nvidia’s revenue in its most recent fiscal year. One institution’s premise has become another’s revenue, and when structures like this are unwound, it is rarely orderly.

The crowd does not want to be deceived, but it needs to belong. Once belonging becomes the point, dissent feels like betrayal to the circle of like-minded believers, and to one’s own social identity.

In traditional markets, fundamentals act like gravity. They cannot prevent bubbles, but they eventually reassert themselves. In gamified markets and certain speculative cycles, this gravity is weakened. Crypto strips away the stabilizers: earnings, balance sheets, and yield are no longer tied to productive activity. When prices rise, it is simply because someone else believes they will rise further, and when they fall, there is nothing underneath to slow the descent.

The European Central Bank has warned that crypto valuations are especially vulnerable to sharp corrections precisely because they are driven by sentiment and leverage rather than intrinsic value. When confidence shifts, volatility spikes and price discovery collapses.

But the distortion is no longer confined to crypto. The S&P 500 is the most visible example of a broader valuation tension. By the end of 2025, the top ten holdings represented 40% of the index’s total weight, the highest level of concentration since at least 1972. The forward P/E of the Magnificent Seven averaged 28 times expected earnings, while the Shiller CAPE ratio exceeded 40 for the first time since the dot-com crash. Last October, NVIDIA alone crossed $5 trillion in market capitalization (within a decade of its AI pivot), cementing its position among the most valuable companies ever recorded and surpassing the GDP of every country except the US and China.

In 2025, just ten stocks, or 2% of the index by count, accounted for roughly 40% of the S&P 500's total weight. The index is doing exactly what a cap-weighted index is designed to do. The question is whether investors holding it understand what they have actually bought.

The tension here is one the market has not resolved: the top ten companies in the S&P 500 are generating roughly 32.5% of the index’s total earnings, up from 17% in 2015. Their dominance is not entirely narrative-driven. But their weight in the index (~40%) materially exceeds their earnings share, implying a valuation premium that requires sustained, exceptional execution to justify. Historical data on high-concentration periods suggests that the top ten following prior concentration peaks, in 1980 and 2000, subsequently underperformed the broader market. That is not a forecast but context that should inform how a long-horizon investor thinks about what passive equity exposure actually represents.

The AI infrastructure question sharpens this tension further. In 2026, hyperscaler capital expenditure on AI infrastructure has surpassed $700 billion (a number that continues to rise), more than five times the enterprise AI revenue it is meant to unlock. A February 2026 NBER study found that despite 90% of firms reporting no measurable AI impact on workplace productivity, executives projected AI would increase productivity by 1.4%. The capital cycle argument that overbuilding eventually produces excess supply, falling returns, and a reckoning with valuations has not been answered, simply deferred.

This is not an argument that AI is not real, or that the technology will not compound meaningfully over time. The distinction that matters, and that the crowd consistently struggles to hold, is between infrastructure and spectacle. Between companies with defensible business models and those relying on the narrative premium granted by proximity to the real thing.

Life of Brian ends without any major in-universe revelation. The crowd drifts away, already scanning for the next story. The underlying joke is not that the crowd was foolish in this specific instance; it is that nothing about its behavior has changed.

The gamified economy presents long-horizon investors with a genuine and unresolved question. It is not whether any of this technology is real, some of it plainly is, with the transformative potential to justify sustained investment. The question is whether current pricing is doing what pricing is supposed to do: rationally allocating capital toward productive uses on the basis of expected future returns, rather than amplifying belief cycles that reward early arrival and punish careful analysis.

There is a structural case that something has shifted durably. Retail participation in options markets, the gamification of trading platforms, and the social-media amplification of narratives are not temporary phenomena. They represent a change in how a meaningful share of market participants engage with financial instruments, as participation tokens in a real-time game, not as claims on productive output. The implications for price formation are not yet fully understood, even by the institutions most directly affected. What is increasingly clear, however, is that the regulatory environment that once provided structural friction against the worst excesses has itself shifted. The SEC’s deregulatory posture since 2025, dropping enforcement actions, broadening access to speculative instruments, and treating meme coins as beyond the securities perimeter, has removed certain guardrails that, however imperfect, previously imposed some cost on the most unbridled risk. Whether a future policy cycle reintroduces that friction, and at what price, remains an open question.

Responsible investing depends on assets that produce durable economic value: recurring cash flows, productivity gains, institutions that allocate risk over time. It rewards stewardship (strong governance, underwriting discipline, capital formation, etc.), not reflexive participation in fast-moving narratives. The gamified economy inverts this logic. Capital becomes a transient bet rather than a long-dated claim on future output. Returns are driven by momentum and exit timing rather than underlying performance.

The core conundrum is one worth sitting with: The crowd that ignores fundamentals is clearly exposed to correction, but those who refuses to engage with narrative-driven markets risk watching fundamentally sound analysis underperform for longer than any model predicted. Both require the respective investor to be clear about what they are actually doing, and why.

Games are optimized for engagement; institutions are optimized for capital formation. At its most gamified edges, the current economy behaves like the former while promising the latter. Most of the time, by the time the crowd realizes the difference, the board has been reset, and another game is already underway.

This commentary is intended for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results. Crewcial Partners is a registered investment adviser.

© 2026 Crewcial Partners. All rights reserved.

11 min read

There are currently more than 60 armed global conflicts around the world, the most of any period since World War II, most recently punctuated by...

At the 2026 World Economic Forum in Davos, President Donald Trump delivered one of the most unusual addresses the gathering had seen in decades. In...

As your go-to source for insightful analysis, we’re also committed to delivering value to your holiday viewing experience. We’ve done the heavy...